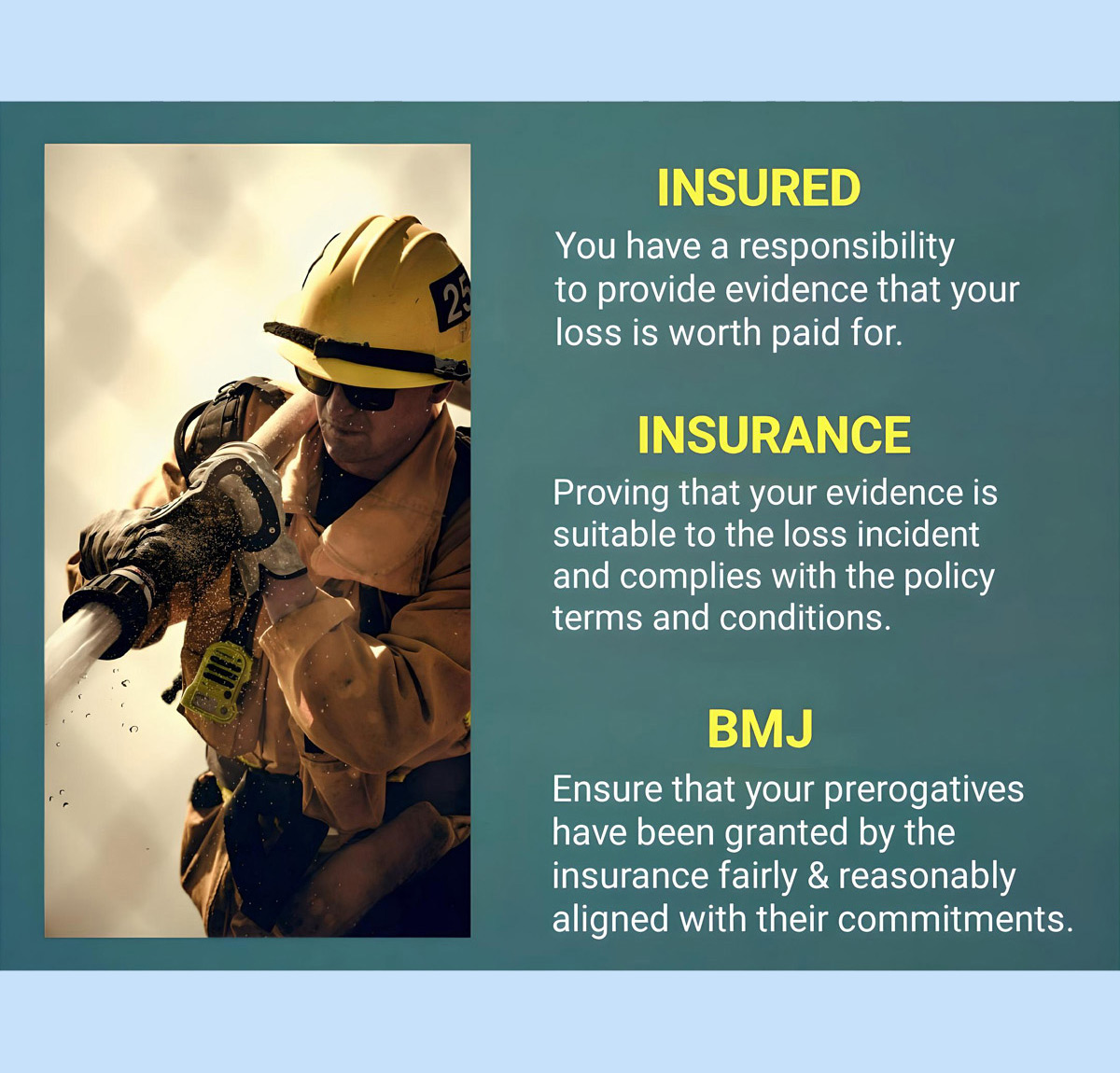

This is because in partial loss claims on Motor Vehicle insurance loss recovery is carried out by the insurance teams.

The insured only provides documents with information related to the incident event, then controls the final result of the repair/ recondition work carried out by the insurance company team, except in certain special circumstances such as the vehicle in a remote area location and the insurer does not have the nearest repair workshop partner located in the insured area, in thi case the insured will supervise the repair/reconditioning process themselves.

It is important to remember, that if the insurance company does not carry out repairs for the loss/ damage you are claiming, they are also not responsible for any impact related to the results of the repair work and/ or the quality of the parts supplied for replacement/ recondition.

Meanwhile, for loss claims on NON Motor Vehicle insurance all loss recovery is carried out by the insured himself, including providing of loss estimation, technicians, mechanics, engineers, repairers, as well as the availability of spare parts and/or materials for the recovery and reconditioning of damage or loss, including the quality and process of carrying out repairs supervised by the insured himself.

The insurance company team only checks the suitability and confirmity of the quantity, quality, price with the related events/ causes of loss and then compares their facts findings with terms and conditions of your insurance policy.

Based on the findings of the facts from the suitability and confirmability assessment, the insurance company will provide recommendations, including details calculation amount as compensation figures for you to implementing recovery losses aligned with terms and conditions of your insurance policy.

If based on the view of insurance that the amount of your claim is considered large and/ or has the possibility of being complicate and disputed, they will appoint other parties to involve as teamwork in an effort to facilitate and convince their re-insurers.

This includes the insurance company will use parties who if possible can deny and/or reject and/or minimize and/ or ensure the amount of loss from the claims that they must pay to the Insured, such as: loss adjusters and/ or surveyors and/or lawyers (advocates), and/or scrap buyers and/or salvors, etc.

We provide attention and care for the fulfillment of your prerogative as an effort to ensure the sustainability of your business toward the future, because the successful fulfillment of client prerogative is our special satisfaction.

We wish our brief explanation helps you understand about the claims process and provides the information you need.

This may mean closing a broken window or door. Authorities officer area i.e police / local security / emergency services must know the situation and conditions, but then you still have to ensure that the building is safe.![]()

This includes boarding up broken windows and doors, and might mean emergency repairs, or covering of the roof if damaged. The fire brigade or police may have even already boarded the property up for you or then seal by police line for couple days.![]()

Never remove any damaged contents as you may need evidence of these for your claim, unless you have official permission from the police and/or insurance you have notified.![]()

Emergency services will handle the situation, but you should ensure the building is safe, secure, and, if possible, secure against theft during and/or after the fire.![]()

This includes sealing damaged windows and doors, and may involve emergency repairs, or covering the roof if damaged (when the loss doesn’t completely destroy the entire building/ premise).![]()

The fire department or police may even have sealed off the property for you, so never remove damaged items, as you may need proof of ownership for your claim.![]()

Once the storm event has passed you should make sure the building is safe, secure and watertight by boarding up any windows and doors and covering any damage to the roof if necessary.![]()

The most important thing is that you do not throw any damaged items away and that you take pictures of the damage where you can. these will all serve as evidence to help with your claim.![]()

In the event of major floods, it might be impossible to keep water outof your buildings, but where possible you should try and sweep or mop the water out and turn any water, gas and electricity services off.![]()

Once cleared, it might also be an idea to place sandbags in external doorways to prevent further flooding if appropriate.![]()

![]()

- Never remove any damaged contents and/or documents related as you may need evidence of these for your claim, except for security reasons from other possible loss amount/ risk that might arise.

- If possible, immediately make documentary evidence of the event or loss that occurred i.e. take some photos and/or videos, because this will make it easier for the implementation of the next stages your claim settlement process.

- In the event of an accident that causes losses to other parties and is suspected to be due to your negligence, do not provide confirmation to them regarding the amount or value of compensation, even though you are convinced that the accident occurred and the loss result that befell the other party was the result of your negligence.

- In the event of a lawsuit for legal liability as a result of your business activities/products or professional work, be patient, don’t panic and tell them that you need time to examine and analyze their lawsuit in more detail and will contact them shortly.

- In the event of a loss, it is clear that you are the one who is negligent resulting in physical material damage and/or bodily injury to third party as motor vehicles case (collision), be patient and tell them that you have insurance coverage against TPL risks and convince the victim (Third Party) that you are responsible and will compensate the loss as soon as the insurance finds out (survey).

(TPL = Third Party Liability). - Do not provide confirmation to them regarding the amount or value of compensation, even though you really believe that the cause of the accident was due to your negligence.

- If there is negligence from other parties that results in losses to you, immediately take action to obtain evidence of their negligence, i.e: confiscation of ID card (if caused by a personal), proof of your official report to their party (corporate), and documents related to the existence of their involvement and then inconsistent with what they had agreed at first the initial outset.

- Report to the police in the nearest area if the accident or loss is due to elements of a criminal motive, i.e: Theft, Burglary, Robbery, Vandalism, etc.

![]()

![]()

This may mean closing a broken window or door. Authorities officer area i.e police / local security / emergency services must know the situation and conditions, but then you still have to ensure that the building and/or locations in your property area is safe.![]()

This includes boarding up broken windows and doors, and might mean emergency repairs, or covering of the roof if damaged. The fire brigade or police may have even already boarded the property up for you or then seal by police line for couple days.![]()

Never remove any damaged contents as you may need evidence of these for your claim, unless you have official permission from the police and/or insurance you have notified.![]()

Emergency services will handle the situation, but you should ensure the building is safe, secure, and, if possible, secure against theft during and/or after the fire.![]()

This includes sealing damaged windows and doors, and may involve emergency repairs, or covering the roof if damaged (when the loss doesn’t completely destroy the entire building/ premise).![]()

The fire department or police may even have sealed off the property for you, so never remove damaged items, as you may need proof of ownership for your claim.![]()

Once the storm event has passed you should make sure the building is safe, secure and watertight by boarding up any windows and doors and covering any damage to the roof if necessary.![]()

The most important thing is that you do not throw any damaged items away and that you take pictures of the damage where you can. these will all serve as evidence to help with your claim.![]()

In the event of major floods, it might be impossible to keep water outof your buildings, but where possible you should try and sweep or mop the water out and turn any water, gas and electricity services off.![]()

Once cleared, it might also be an idea to place sandbags in external doorways to prevent further flooding if appropriate.![]()

![]()

- Never remove any damaged contents and/or documents related as you may need evidence of these for your claim, except for security reasons from other possible loss amount/ risk that might arise.

- If possible, immediately make documentary evidence of the event or loss that occurred i.e. take some photos and/or videos, because this will make it easier for the implementation of the next stages your claim settlement process.

- In the event of an accident that causes losses to other parties and is suspected to be due to your negligence, do not provide confirmation to them regarding the amount or value of compensation, even though you are convinced that the accident occurred and the loss result that befell the other party was the result of your negligence.

- In the event of a lawsuit for legal liability as a result of your business activities/products or professional work, be patient, don’t panic and tell them that you need time to examine and analyze their lawsuit in more detail and will contact them shortly.

- In the event of a loss, it is clear that you are the one who is negligent resulting in physical material damage and/or bodily injury to third party as motor vehicles case (collision), be patient and tell them that you have insurance coverage against TPL risks and convince the victim (Third Party) that you are responsible and will compensate the loss as soon as the insurance finds out (survey).

(TPL = Third Party Liability). - Do not provide confirmation to them regarding the amount or value of compensation, even though you really believe that the cause of the accident was due to your negligence.

- If there is negligence from other parties that results in losses to you, immediately take action to obtain evidence of their negligence, i.e: confiscation of ID card (if caused by a personal), proof of your official report to their party (corporate), and documents related to the existence of their involvement and then inconsistent with what they had agreed at first the initial outset.

- Report to the police in the nearest area if the accident or loss is due to elements of a criminal motive, i.e: Theft, Burglary, Robbery, Vandalism, etc.

![]()

![]()

Keep calm and inform the BMJ officer in chronological detail from the beginning of the activities carried out by the witness and/ or youself until the loss incident occurred.

Mention the names of witnesses and/ or yourself who directly saw, heard and/or were involved in the loss incident event and also are known to have been involved at the scene, including the precautions and security measures taken to prevent the loss becoming large.![]()

![]()

When a survey is carried out by insurance, they sometimes ask you to fill out a claim form as a substitute for submitting an official claim from you.![]()

Please don’t fill in a claims form until we has advised you to do so.![]()

We will tell you know exactly which one you need to fill in, and help you with any parts that you might find difficult.

With you having carried out all the steps above, you have finished making a claim or the first stage of the claim settlement process has been completed and you will be guided by our team to proceed to the next stage in preparing your claim supporting documents according to the loss event that occurred and the type of coverage your policy.![]()

Your claim payments will be subject to an average underinsured calculation, if it is proven that your Sum Insured is lower (inadequate) than the price required by the terms of the insurance policy.

Example :

Terms of the Insurers’ policy Coverage is subject to the New Replacement Value (NRV) for Sum Insured.

It means, the Price of a new good item is required as the Sum Insured of the insurer’s policy, so that if a loss occurs, the insurer can provides you with loss replacement money at a NEW Price, even though the goods covered by the insurer are for OLD goods condition.

This is because the insurance company assumes you pay a premium based on a new price calculation in order to get a new price item replaced when the accident event occur.

However, when your claim is known that the sum insured is Not based on the new price, of course the insurance will Not replace to you with the new price, because you are paying the premium also Not based on the new price calculation.![]()

![]()

Let’s say : the new price is USD 100 million, but your insurance sum insured amount is only USD 75 million (the percentage between the new price and your insurance value is 75%, thereby the premium amount you pay is also only 75%).

Considering that your policy coverage is “not adequate” as the new price (only 75%), of course the insurance only pays you 75% as a claim settlement, or in other words your claim payment will be deducted by 25% as an average calculation due to your policy coverage is “under insured”.

However, the above conditions (new for old payment) are subject to the New Price of the replacement item having the same level of quality and quantity as the claimed to old damaged item, otherwise they will deduct as a “Bettement Factor” to your claim payment.

Insurance will deduct as “betterment factor” from your claim payment calculation, if you replace a damaged item with a better quality item than the one covered by the policy.

This is because the NEW replacement price for your claim covered by the policy must be of the same quality and/ or quantity as the damaged/ loss item you claimed.

![]()

![]()

If the quality and/ or quantity are not equal, thereby the difference between the two prices is excluded and not covered by the insurance.

Insurance make deduction to your claim amount by a “betterment factor” because the premium you pay is equal to the price for the item with quality and/ or quantity covered by the policy.

BMJ Insurance Brokers

![]()

Registered and supervised by

The Financial Services Authorities

Of The Republic Of Indonesia (OJK RI)![]()

License No. KEP-424/KM.5/2005![]()

![]()

![]()

Member of

The Association of Indonesian Insurance

And Reinsurance Broking Companies

(APPARINDO)![]()

![]()

QUICK LINKS